Looking at the Future of Bitcoin... Backwards?

Looking at the Future of Bitcoin... Backwards?

Executing a Carry Trade to Profit off Bitcoin Futures in Backwardation

Welcome to the 189 new investors joining us since last Monday. If you’re reading this, but haven’t subscribed, join our family of 681 smart, growth-mindset folks here!

If you enjoy or get value from Investing Lessons, consider helping me reach 1,000 subscribers by the end of June (my birthday!) by doing any of the following:

Forwarding this post to friends, and getting them to subscribe.

Sharing on Twitter, Facebook, and Linkedin with a note of what you learned.

Sharing within community or company Discord/Slack/Facebook groups.

Make some tea. 🍵

Today, you will learn to execute a ‘carry trade’, by exploiting a phenomenon known as a ‘backwardation’ in the Bitcoin futures market. Last month presented many such opportunities, allowing one to profit in an almost risk-free manner.

To those wondering, the final part in the Untold Story of Options Trading Trilogy will be released next week. If you haven’t read the first two parts, links are provided below:

🇬🇷 The Humble Greek Origins of Options Trading (Pt1)

🎲 How Black Scholes Precipitated the 1987 Black Monday (Pt2)

🔮 What is a Future…?

Most of you should know that you can purchase Bitcoins (BTC) directly on an exchange. Upon paying a certain price, also known as the spot price, you will receive ownership of the Bitcoin immediately.

But what happens if you don’t want Bitcoins right now, but at some time in the future?

A future contract still allows you to purchase Bitcoin for a particular price. However, settlement is now at some time in the future at a specified delivery date.

Traditionally futures were underwritten for commodities. At the delivery date, the two parties involved would exchange physical commodity goods at a predetermined price.

For cryptocurrencies most futures are cash-settled rather than physically-settled. This means that no physical Bitcoins are exchanged. Instead settlement involves only a cash payment, thereby avoiding transactional or transportational fees.

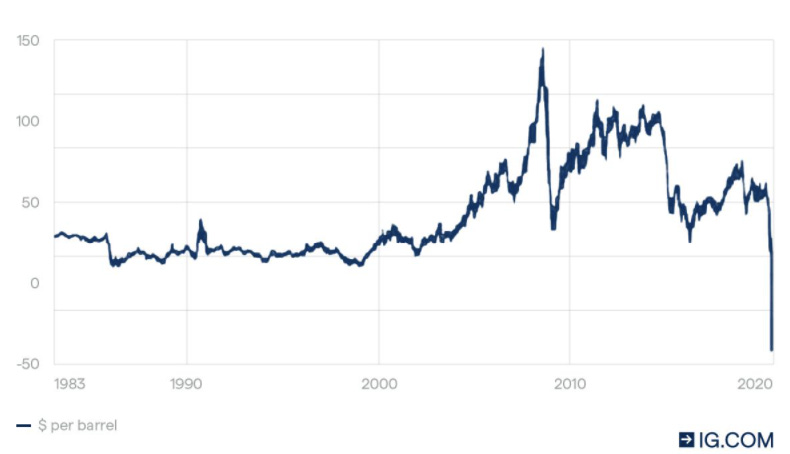

How futures are settled is a subtle, but important detail. Crude oil such as WTI future contracts are physically settled, but the unavailability of storage space caused oil to plummet to negative prices in 2020. Here the cost of last-minute storage space exceeded the cost of oil.

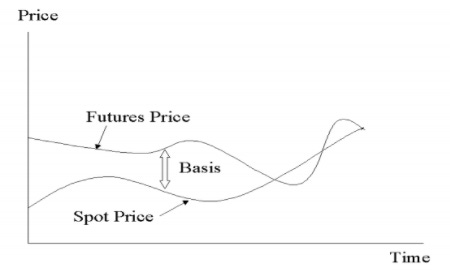

One can easily see that the futures and spot price should diverge from each other prior to the delivery date, as we need to consider the cost of carry. This accounts for the borrowing interest rate to fund the position (typically zero-risk rate), plus any additional costs including transportation, storage, and transactional. Any dividend coupon payments are also subtracted, as it reduces your cost to carry or hold the investment,

At the delivery date, it is worth noting that the future price should theoretically converge onto the spot price (especially if it is cash-settled). Practically this is not always the case, as there exists settlement risk when delivering the physical product such as in the WTI oil case study.

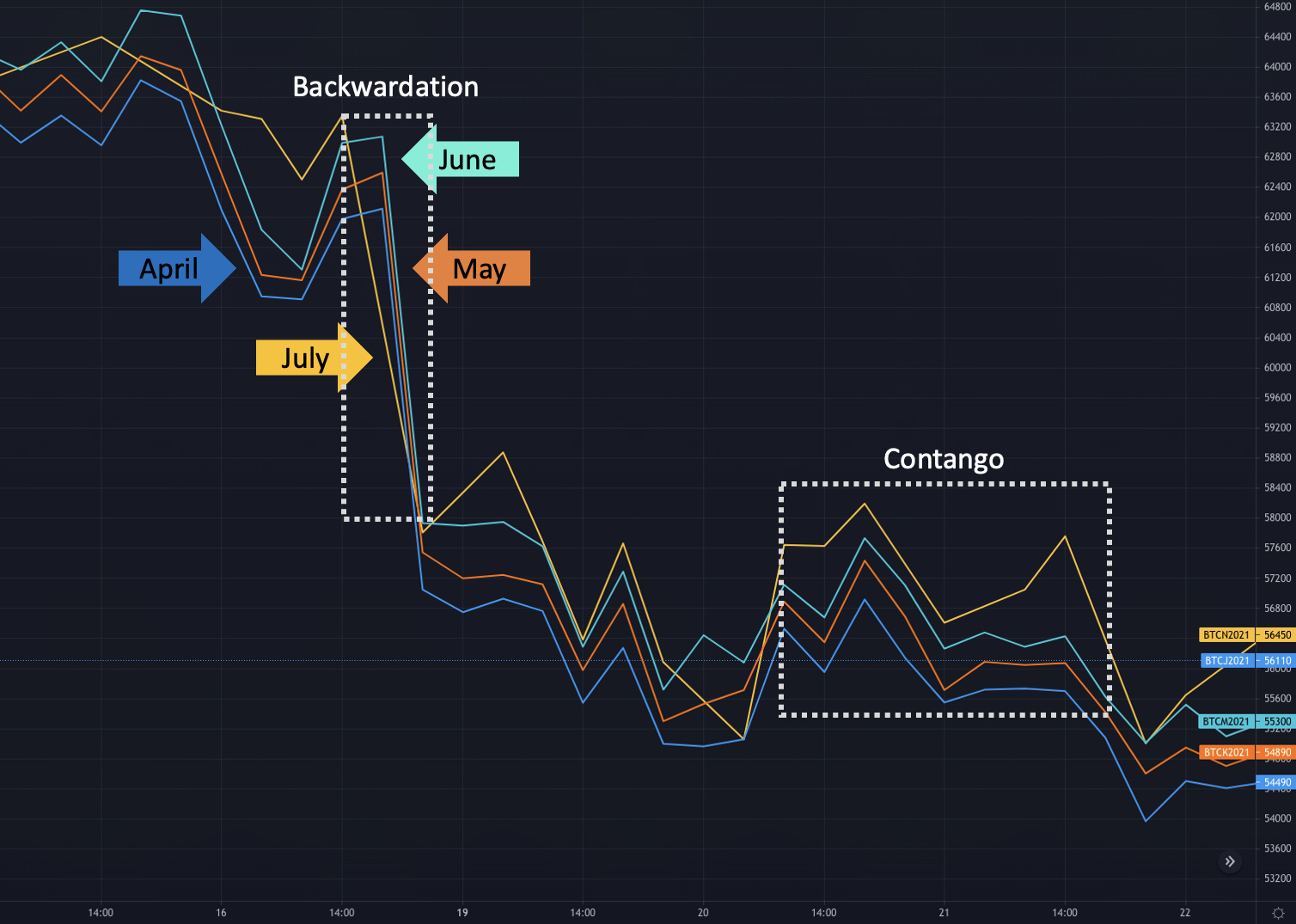

📊 Backwardation and Contango Explained

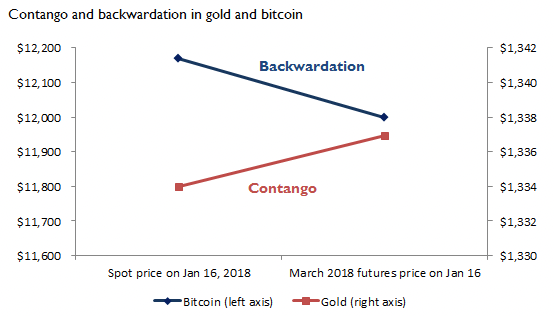

Contango occurs when the futures price is greater than the spot price. This is the normal situation, as there is typically a cost of carry associated with holding an asset.

Backwardation is the exact opposite, occurring when the spot price is greater than the futures price. This typically occurs when there is a higher demand for an asset in the short-term, such as a shortage in supply.

📈 Placing a Bitcoin Carry Trade

Yield Farming of up to 50% with Contango Carry Trades

During a contango, one can place a bet on the cost of carry, by placing the following trades:

Long Bitcoin Spot for $58,000 in April

Short Bitcoin July Futures at $61,500

The net result of such a trade, would be being short the cost of carry (one can think of futures as the spot plus the carry). If this spread further widens you will lose money, and vice versa. Additionally as you are offsetting Bitcoins with each other, you are now hedged from any Bitcoin price fluctuations - we call this being delta neutral.

The cost of carry behaves exactly like the price of a stock. If the cost of carry goes down, the trader can choose to close the entire position for a quick profit. On the contrary if the spread increases, your capital is now locked up as you need to hold the position until expiry, wait for the spread to collapse again, or sell at a loss.

If the trader chooses to hold the position until delivery date, recall that the futures and spot prices should theoretically converge on one another. Practically as most cryptocurrency contracts are cash-settled, there are very minimal settlement risks to do with transportation or storage. Some potential risks may include counterparty risks, increased margin or trading fees.

The above trade should theoretically yield us $3,500 on a $61,500 collateral. That is almost a 6% yield in 4 months, or 19% annualised - practically risk free! At the peak of crypto mania, I have seen annualised rates of over 50%. Talk about free money.

With further market efficiencies from institutional and DeFi auto market makers, the yield curves in the cryptocurrency universe should stabilise. There are plenty of trading opportunities available due to mispricings on yield premiums between futures of different expiry dates.

Backwardation Carry Arbitrage in Cryptocurrency Futures

While the contango carry trade is great for elevated yields of above 15%, backwardation in the realm of cryptocurrencies is effectively free cash. Due to crypto futures being cash-settled, there are no risks associated with physical-settled contracts. It is likely that backwardation occurs as a result of large liquidations from auto-deleveraging mechanisms, rather than a market anomaly.

Backwardation mispricing opportunities when presented should only last for a short time, before being arbitraged out. Once again with more efficient markets, these opportunities should become rarer.

Here is an example of a backwardation trade in April

Long Bitcoin July Futures for $60,000

Short Bitcoin Spot at $63,500

In this situation, you are purchasing the cost of carry for -$3500. A negative cost of carry means that the price of borrowing money is higher than the returns earned on the borrowed money. As backwardations are merely a mispricing in the market, this phenomenon typically reverses itself back into a contango.

Had this backwardation trade reversed into the above contango example, you would have profited $7,000 after closing out the position.

Disclosure

It should be noted that this is not financial advice, and you certainly shouldn’t implement such a strategy into the bond, commodities or currency futures market blindly. These markets are typically physically-settled, so they contain additional risks not discussed in this newsletter. Furthermore these markets are much more efficient, so there are also less no-brainer opportunities.

💭 Market Musings

Here is a hypothetical trade to profit off negative oil prices in the example above, when there were a shortage of storage facilities for the physical settlement of oil.

Buy 2 million barrels of crude oil for -$50. You now have $100M.

You rent a VLCC oil tanker for $40,000/day, that can store 2M oil barrels

You charter the tanker for half a year, as oil prices recover. Rent and charter expenses should cost you ~$10M.

Sell oil barrels for $30. Your net profit is $100M - $10M + $60M = $150M.